Capital Budgeting

Capital Budgeting Introduction

Capital budgeting is the process of evaluating and selecting long-term investment projects or expenditures that involve significant capital outlays. It is a critical financial management tool used by businesses to make informed decisions about allocating their financial resources for projects that will yield returns over an extended period.

What Is Capital Budgeting?

Capital budgeting involves analyzing potential investment opportunities and determining whether they align with a company's strategic objectives and financial goals. It considers the inflow and outflow of cash over the life of a project to assess its profitability and viability.

The Importance Of Capital Budgeting For Businesses

Capital budgeting plays a vital role in business decision-making for several reasons:

- Allocation of Resources: It helps businesses allocate limited financial resources to projects that offer the highest potential for long-term profitability and growth.

- Risk Assessment: Capital budgeting techniques allow businesses to evaluate the risks associated with investment projects, ensuring that the selected projects align with the company's risk tolerance and return objectives.

- Strategic Planning: Capital budgeting facilitates strategic planning by identifying investment opportunities that align with the company's long-term goals and vision.

- Efficient Resource Utilization: By systematically evaluating and selecting projects, capital budgeting ensures that financial resources are utilized efficiently and effectively.

- Value Creation: Successful capital budgeting leads to value creation for the business by selecting projects with positive net present value (NPV) and generating sustainable cash flows.

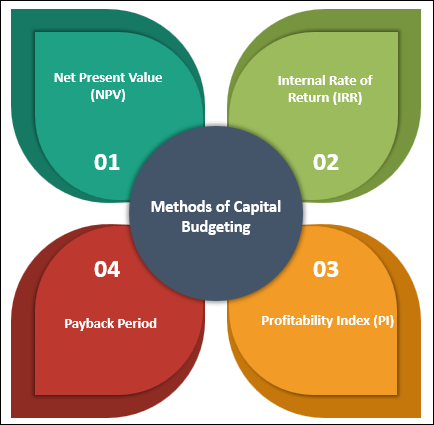

Methods Of Capital Budgeting

Several methods are used in capital budgeting to evaluate investment projects, including :

- Net Present Value (NPV): NPV compares the present value of cash inflows to the present value of cash outflows, considering the time value of money. Positive NPV indicates that the project is expected to generate more cash inflows than outflows and is considered desirable.

- Internal Rate of Return (IRR): IRR is the discount rate that equates the present value of cash inflows with the present value of cash outflows. It represents the project's rate of return. Projects with an IRR higher than the required rate of return are typically considered favorable.

- Payback Period: Payback period measures the time required for the project's cash inflows to recover the initial investment. It provides an indication of the project's risk and liquidity but does not account for cash flows beyond the payback period.

- Profitability Index (PI): PI is the ratio of the present value of cash inflows to the present value of cash outflows. It measures the value created per unit of investment and helps rank projects based on their relative profitability.

Factors To Consider When Implementing A Capital Budget

When implementing a capital budget, businesses should consider the following factors:

- Project Viability: Evaluate the financial feasibility, market potential, and technical aspects of the project.

- Risk Assessment: Assess the risks associated with the project, including market risks, operational risks, and financial risks.

- Cash Flow Projections: Develop realistic cash flow projections, considering the timing and magnitude of cash inflows and outflows throughout the project's life.

- Cost of Capital: Determine the appropriate discount rate or cost of capital to evaluate the project's profitability.

- Strategic Fit: Evaluate how the project aligns with the company's strategic objectives, long-term plans, and risk appetite.

- Regulatory and Environmental Considerations: Consider any regulatory or environmental requirements that may impact the project's implementation or operations.

Advantages And Disadvantages Of Capital Budgeting

Advantages of capital budgeting include:

- Improved Decision-making: It provides a structured approach to evaluate and prioritize investment projects, leading to better decision-making.

- Resource Allocation: It ensures that financial resources are allocated to projects with the highest potential return, improving resource utilization.

- Long-term Planning: Capital budgeting supports long-term strategic planning by assessing the impact of investment decisions on the company's future.

- Risk Management: It helps businesses assess and mitigate risks associated with investment projects.

Disadvantages of capital budgeting include:

- Complexity: The evaluation and analysis involved in capital budgeting can be complex and time-consuming.

- Uncertainty: Future cash flows, market conditions, and project outcomes can be uncertain, making it challenging to accurately predict project performance.

- Information Limitations: Capital budgeting relies on accurate and reliable information. Inaccurate or incomplete data can lead to flawed decision-making.

- Costly Mistakes: Poor capital budgeting decisions can result in substantial financial losses for the business.

Conclusion :

Capital budgeting is a fundamental process for businesses to make investment decisions that align with their strategic goals and financial objectives. It ensures efficient resource allocation, risk assessment, and long-term value creation. By using appropriate capital budgeting methods and considering key factors, businesses can improve decision-making, optimize resource utilization, and enhance their overall financial performance.